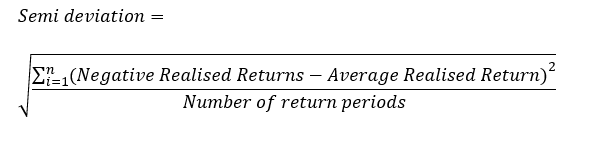

The Sortino ratio measures the excess returns earned per unit of downside risk (negative returns within the investment period). The excess returns are the difference between realised returns earned on the Account, and a risk-free rate (best risk-free alternative to investing such as holding cash). Saxo Bank uses a risk-free rate of zero and calculates Sortino Ratio for a period of at least 6 months. To measure the risk taken over a year, downside risk takes into account, only the days where a loss has occurred during the period. The downside risk is the standard deviation of negative returns (semi deviation) and is focused on returns that fall below target return (the average return). The downside deviation is calculated as:

Assume a realised return of 6% and a risk-free rate of 0%, with a downside deviation of 13%. The Sortino ratio for the period is:

A high Sortino ratio indicates that the risk taken on the Account is being rewarded in the form of higher percentage returns. The higher the Sortino ratio, the better the Account’s returns have been over the year being measured, in relation to the downside risk (losses) observed in the investment period.