Standard deviation is the measure of investment risk and return, and the amount by which returns deviate from the average return observed within the investment period. The variance (deviation from the average return) of the returns is an indication of volatility (fluctuation), and the risk undertaken to achieve those returns. It becomes relevant when assessing historical returns as a deterministic measure of expected future returns, in relation to the risk assumed. The following steps are taken to calculate the standard deviation:

Arithmetic Mean

If returns were measured every month over a period of six months then the average return (arithmetic mean) in the investment period would be calculated as:

Variance

The variance of the returns would be a spread of the returns around the arithmetic mean (7.5%, which is the average return observed in the investment period). The variance is calculated as the difference between each return in the year, and the average return (7.5%). The difference between the return observed and the average return is squared, to find the variance. This adds weight to those results that are furthest from the average return. The outliers are significant when measuring the dispersion of returns, therefore squaring the deviations ensures that the values above the average return to do not cancel out those values below the average return. The sum of the variance of all the returns is calculated as:

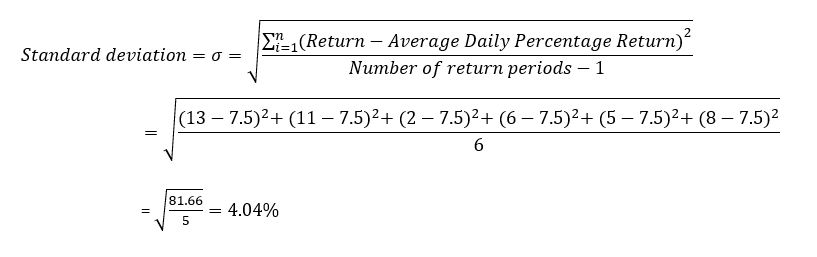

Standard Deviation

To determine the norm of these returns (information about how dispersed the returns are), the standard deviation is calculated as the square root of the variance. This gives the average amount by which the returns over the six month period, deviate from the average return. The higher the standard deviation of returns, the higher the volatility of returns (greater fluctuation in the returns observed in the investment period). High volatility indicates that high risk was undertaken during the investment period.

Standard deviation informs us about the dispersion of returns relative to the average return, and the normal range of returns that can be expected to be observed. With an average return of 7.5% and a standard deviation of 4.04%, returns can be expected to lie between 3.46% (7.5% - 4.04%) and 11.54% (7.5% + 4.04%).

Saxo calculates standard deviation on daily returns.